I wonder how, in the long-run, people will respond to this. On the one hand, the favorite trope of many is that markets fail, particularly insurance markets, because of the asymmetric information problem. On the other hand, there are always going to be huge concerns about privacy when it comes to the many solutions like this one to the problem.

More to say, as always.

As one of the initial designers of using these devices in insurance back in the aughts (I am since retired), let me chime in.

In our market testing we found that consumers would only join the program if the program had only upside potential. In other words they will join to get a potential discount as long as there is no chance of a surcharge. So that is of course how we built the program (I did not work at SF). It can encourage safe driving, can provide feedback on safer driving habits, and is a competitive must have as it effectively attracts better drivers to the program.

As with all things economic, it is what is not seen which is also critical. Note that those NOT joining the program (and the competitors not offering the service) will tend to have higher usage and worse driving experience. This will effectively increase base rates over time and increase the discounts and advantages of joining the program. Eventually, it will be extremely expensive to NOT join a similar type of program. It is all a matter of time, and my guess is few if any companies will use anything other than discounts (carrots) to get there.

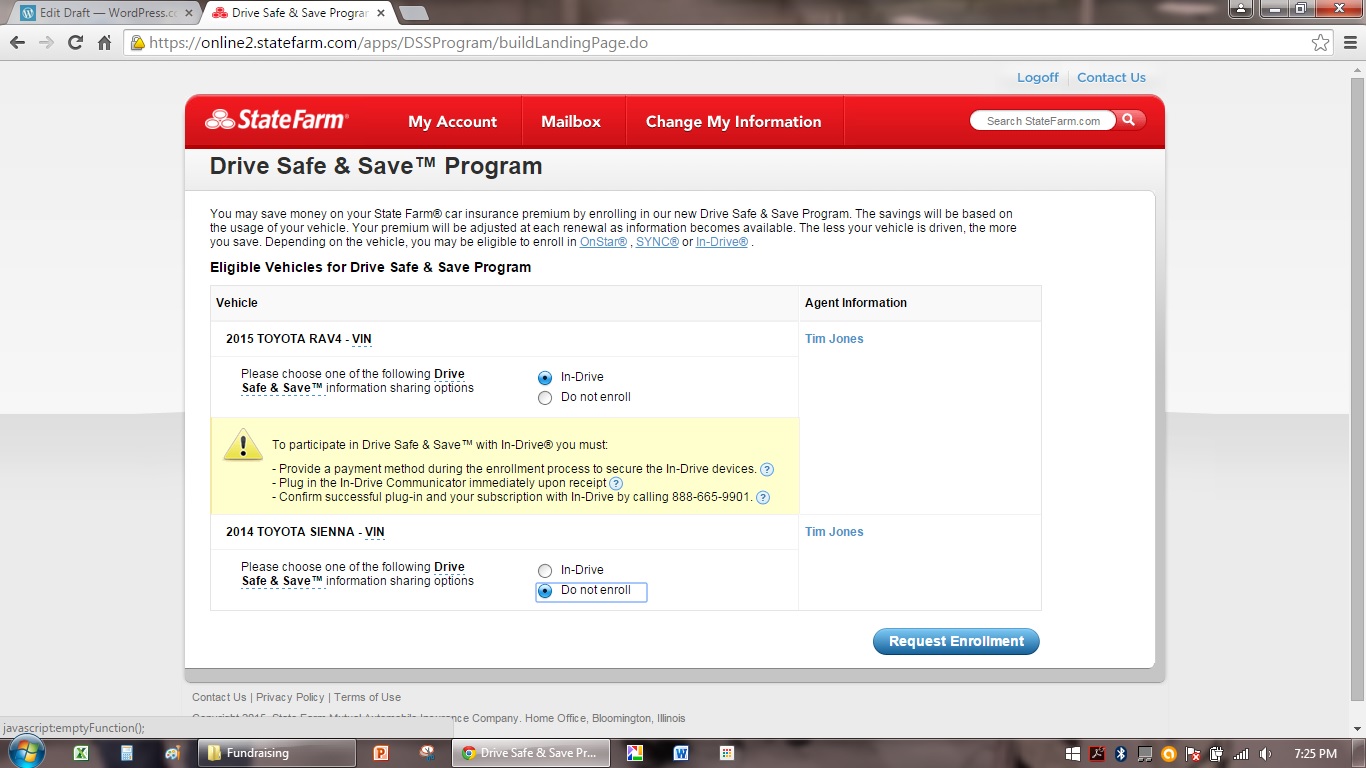

Thanks. In this iteration, State Farm actually warns us that there are some events that may trigger rate increases. I signed up anyway of course. When this technology works perfectly as you outline, I look forward to the blog post that merely says, “And then there is health insurance …”

I have strong beliefs that we can do very well at placing health care customers into pretty well defined risk bins, it’s just that people have no tolerance for such things.